The Credit Score Myth That’s Holding Would-Be Buyers Back

Would-be homebuyers aren’t sitting on the sidelines because they don’t want to buy. They’re sitting out because they think they can’t. And sometimes, it’s their credit score that’s holding them back.

According to a Bankratesurvey, 2 out of every 5 (42%) Americans believe you need excellent credit to qualify for a mortgage. That may be why, when renters are asked why they don’t own yet, “my credit isn’t good enough” comes up often.

Maybe you’re in the same boat. You look at your score, see it’s not where you want it to be, and assume buying your first place just isn’t realistic right now.

But here’s what you need to know.

Even though a lot of people assume you need flawless credit to buy a house, that’s not necessarily the case.

You Don’t Need Perfect Credit To Buy a Home

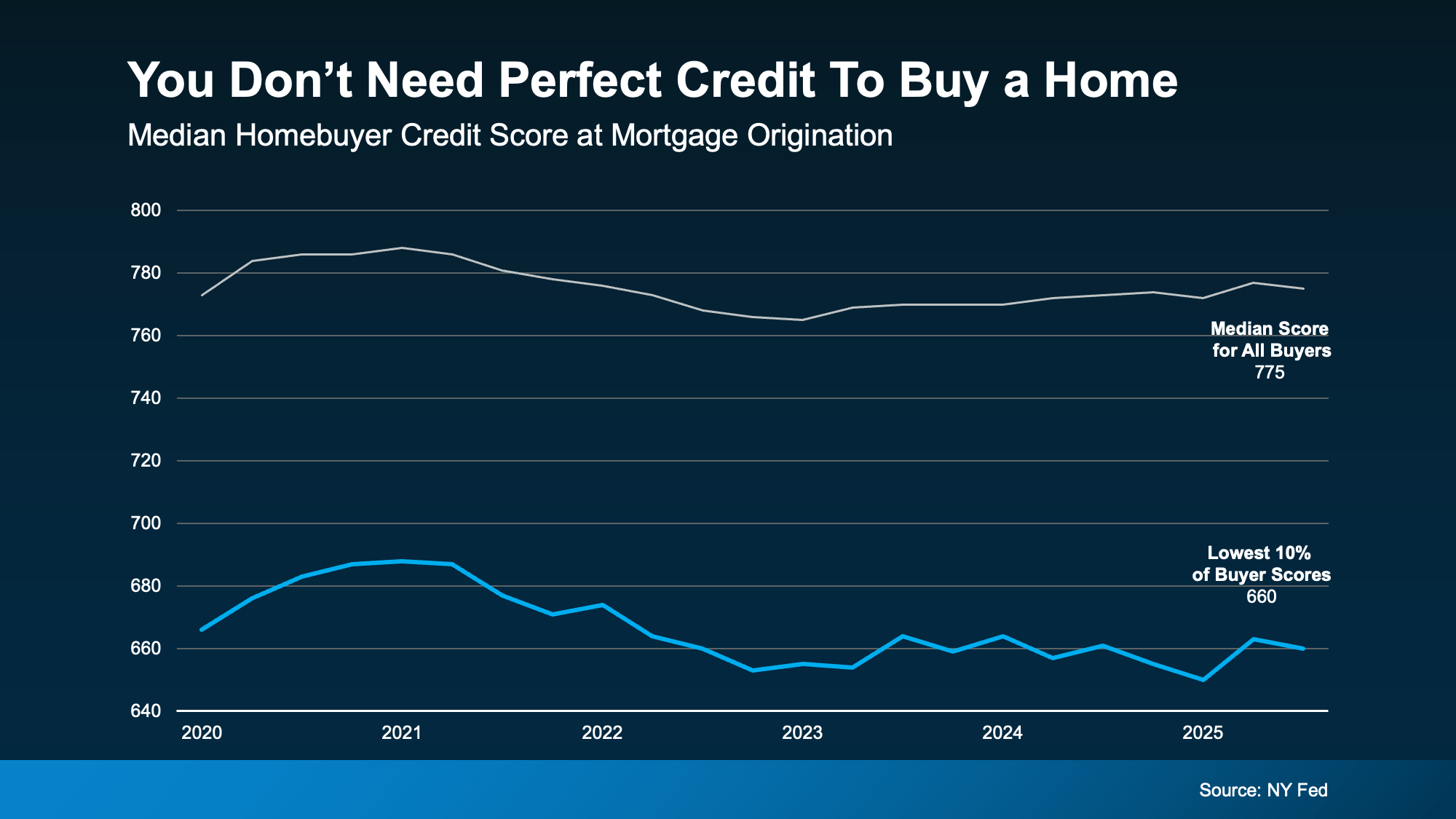

So, where’s this myth come from? Part of the confusion stems from the fact that the typical homebuyer today does have a fairly strong credit score. In fact, according to data from the NY Fed, the median credit score for all buyers is 775.

But that doesn’t mean you need a score that high to qualify.

Looking at recent homebuyers, a number were able to get a mortgage with scores below that threshold. Data shows 10% of scores were around 660. Which means some were higher than that and some were lower, but the median in that lowest 10th percentile was around that range (see graph below):

So, even if your score isn’t as high as you want, that doesn’t automatically close the door. FICO explains there is no universal credit score you absolutely have to have when buying a home:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use . . .”

The best thing to do is to talk to a trusted lender to see what’s possible for you. Because a portion of buyers are buying with scores in the 600s – and maybe that means you can too.

Bottom Line

Your credit score is important. But that doesn’t mean it has to be perfect.

If credit has been the reason you’ve been waiting to buy a home, it might be time to take another look at your options. If you want help understanding where you stand and what your next step could be, connect with a local lender.

You don’t need to have everything figured out to start the conversation.

Expert Forecasts Point to Affordability Improving in 2026

Wondering what to expect from the housing market in 2026? You’re not the only one. For the past few years, affordability has been the biggest barrier standing between most people and their next move. And a lot of buyers and sellers have been holding their breath waiting for things to get better. The good news? It’s finally happening.

In 2025, affordability was the best it’s been in 3 years. And experts agree the momentum will keep going in 2026. And that’s based on their analysis of the key factors shaping the housing market in the year ahead: mortgage rates, inventory, and home prices.

Lower Mortgage Rates Are Already Here

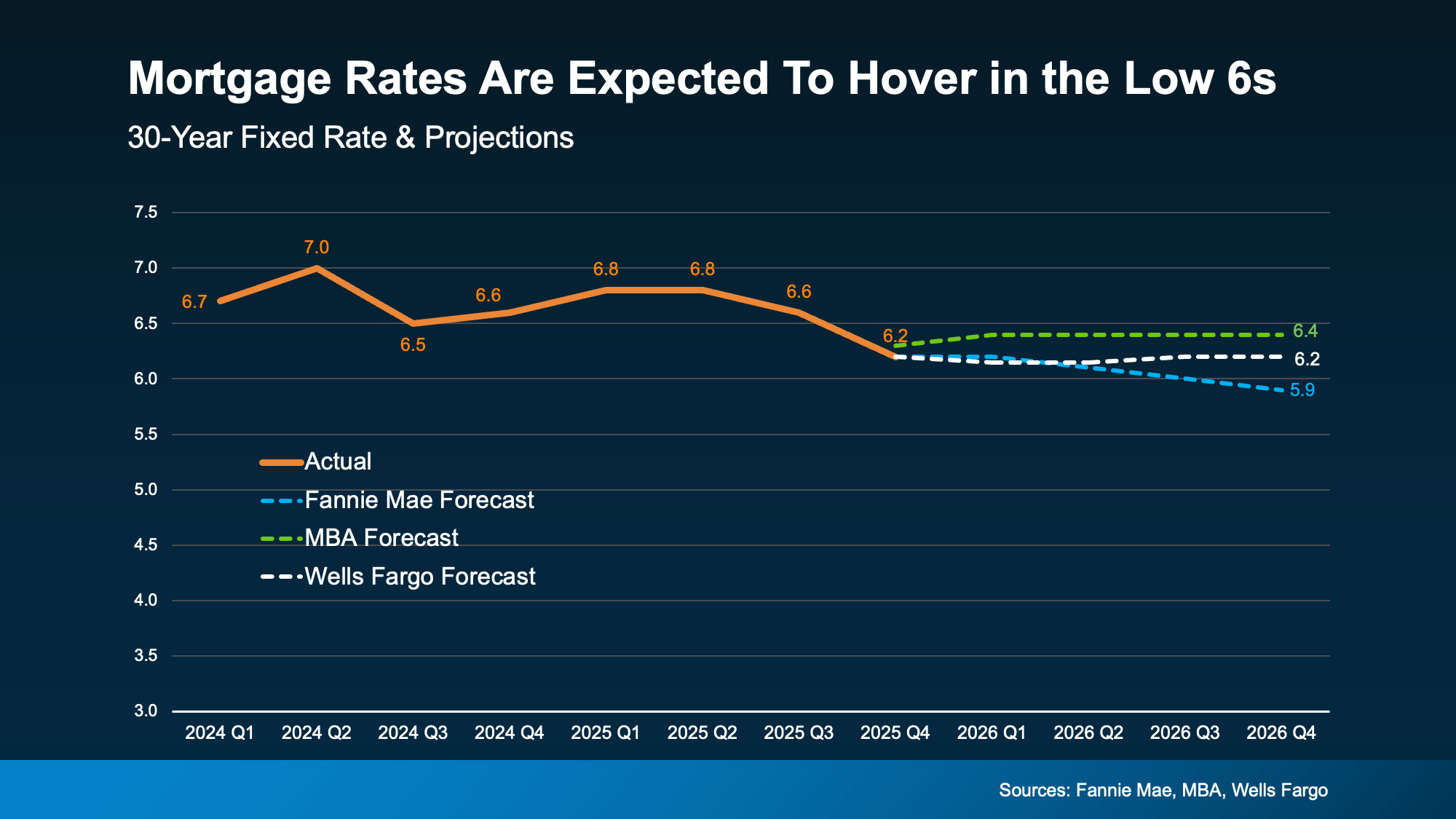

Mortgage rates have already come down from their peak. By some counts, they dropped by almost a full percentage point over the course of the last year. And that’s a big deal, even if it doesn’t sound like it. But how low will they go? And should you wait for them to come down more? Here’s your answer.

Forecasts suggest they’ll stay pretty much where they are now and hover in the low 6% range throughout 2026 (see graph below):

Where they go from here really depends on what happens with the economy, the job market, and any changes in monetary policy the Fed makes in the year ahead. The important thing is, they’re already lower than they were just one year ago and that’s ideal if you’re planning a 2026 move.

For buyers: A lower rate reduces monthly payments and increases buying power. And, that combo helps more people qualify for homes that previously felt just out of reach.

For sellers: It may be time to accept that rates in the 6s are the new normal. And if you need to move, it’s doable, especially with your equity.

Even More Options Are on the Way

In 2025, the number of homes for sale improved by about 15%. As inventory rose, buyers regained things they hadn’t had in years: options, time to consider those options, and negotiating leverage. That helped restore more balance to the housing market.

Not to mention, the inventory gains are a big piece of what’s helped price growth slow down – which in turn improves affordability.

While the inventory gains this year aren’t expected to be as steep, experts at Realtor.comsaythe supply of homes for sale should grow by another 8.9% this year.

For buyers: That means even more choice and more negotiating power.

For sellers: Pricing your house right will be essential to draw in buyers.

Home Price Growth Is Slowing to a More Sustainable Pace

With more homes for sale, there isn’t as much upward pressure on prices right now. And we’ve seen that shake out over the past year. Even so, the overwhelming majority of experts say, nationally, prices will continue rising in the year ahead – just at a slower pace. On average, they say prices will rise by 1.6% in 2026 (see graph below):

And that’s reassuring if you’ve been fed content on social media saying prices are going to come crashing down. But here’s what you need to remember most about this. It’s going to vary a lot by area.

So, lean on a local agent for the latest on what’s happening where you are. Some markets will see prices rise more than this. Others may see prices come down slightly. It really all depends on conditions in your local market

But overall, prices will continue to rise at the national level. And that’s good for the market as a whole. As Realtor.comexplains:

“For homebuyers and sellers, the shift signals a more balanced market—one where price growth steadies, rate relief offers breathing room, and negotiating power tilts subtly toward buyers.”

For buyers: Expect more moderate price growth, not the sudden and intense spikes just a few short years ago. That gives you fewer surprises and more predictability, which makes budgeting a whole lot easier.

For sellers: This slower price growth restores balance without putting your equity at risk. And that’s a win.

More Homes Will Sell

All of this adds up to a better affordability equation in 2026. And that’s exactly why experts are saying we should see more homes sell (and more people buy) this year.

As Mischa Fisher, Chief Economist at Zillow, says:

“Buyers are benefiting from more inventory and improved affordability, while sellers are seeing price stability and more consistent demand. Each group should have a bit more breathing room in 2026.”

The bottom line is, more people are finally going to be able to make their move this year. So, the question is: will you be one of them? The market is giving you an opportunity you haven’t had in a while. Maybe it’s time to take advantage of it.

Bottom Line

Affordability won’t change suddenly overnight. But, with several key trends working together, it should slowly and steadily improve in the months ahead.

That’s exactly why, in 2026, you should see a market with more balance, more predictability, and more breathing room than you’ve had in years.

Want more information about the opportunities unlocking in our local market?

Thinking about Selling Your House As-Is? Read This First.

If you’re thinking about selling your house this year, you may be torn between two options:

Do you sell it as-is and make it easier on yourself? No repairs. No effort.

Or do you fix it up a bit first – so it shows well and sells for as much as possible?

In 2026, that decision matters more than it used to. Here’s what you need to know.

More Competition Means Your Home’s Condition Is More Important Again

Over the past year, the number of homes for sale has been climbing. And this year, a Realtor.com forecast says it could go up another 8.9%. That matters. As buyers gain more options, they also re-gain the ability to be selective. So, the details are starting to count again.

That’s one reason most sellers choose to make some updates before listing.

According to a recent study from the National Association of Realtors (NAR), two-thirds of sellers (65%) completed minor repairs or improvements before selling (the blue and the green in the chart below). And only one-third (35%) sold as-is:

What Selling As-Is Really Means

Selling as-is means you’re signaling upfront that you won’t handle repairs before listing or negotiate fixes after inspection. That can definitely simplify things on your end, but it also narrows your buyer pool.

Homes that are move-in ready typically attract more buyers and stronger offers. On the flip side, when a home needs work, fewer buyers are willing to take it on. That can mean fewer showings, fewer offers, more time on the market, and often a lower final price.

It doesn’t mean your house won’t sell – it just means it may not sell for as much as it could have.

How an Agent Can Help

So, what should you do? The answer isn’t one-size-fits-all. It’s going to depend a lot on your house and your local market.

And that’s why working with an agent is a must. The right agent will help you weigh your options and anticipate what your house may sell for either way – and that can be a key factor in your final decision.

If you choose to sell as-is: They’ll call attention to the best features, like the location, size, and more, so it’s easy for buyers to see the potential, not just the projects.

If you decide to make repairs: Your agent can pinpoint what’s really worth the time and effort based on your budget and what buyers care about the most.

The good news is, there’s still time to get repairs done. Typically speaking, the spring is the peak homebuying season, so there are still several months left before buyer demand will be at its seasonal high. That means you have time to make some repairs, without rushing or stressing, and still hit the listing sweet spot.

The choice is yours. No matter what you end up picking, your agent will market your house to draw in as many buyers as possible. And in today’s market, that expertise is going to be worth it.

Bottom Line

While selling as-is can still make sense in certain situations, in some markets today, it may cost you. So, no, you don’t have to make repairs before you list. But you may want to.

To make sure you’re considering all your options and making the best choice possible, let’s have a quick conversation about your house.

Why Pre-Approval Should Be Your First Step – Not an Afterthought

Finding the right home feels exciting – but being pre-approved for your loan is what makes it possible. Whether you’re planning to buy soon or still just thinking about it, getting pre-approved is one of the best moves you can make. Here’s why.

1. What Is Pre-Approval, Really?

Pre-approval is much more than a guess. It means a lender has reviewed your finances (things like your income, assets, credit score, debts, and savings) and told you how much they’re willing to let you borrow for your loan.

It’s basically a reality check for your home search, so you can make sure it aligns with your budget and shop confidently when you’re ready to go.

2. Why It’s a Power Move (Especially Right Now)

The housing market’s been shifting lately with mortgage rates moving, prices moderating, and inventory rising. So, knowing what you’re working with in the current market is a big reason why pre-approval matters. Here’s what it gives you:

Clarity: You’ll know what you can afford before you fall in love with a house that’s potentially out of reach.

Confidence: Sellers will take your offer seriously when they see you’re pre-approved because you’re not a risky buyer.

Control: If rates come down and you want to jump on the moment, you’re already a step ahead with your plan.

As Experian explains:

“. . . you’ll want to make sure you receive your preapproval letter before you start looking at homes so you can submit a strong offer as soon as you find what you want. The process can take anywhere from a day to a few weeks, so if you procrastinate, you may lose out to a competing offer.”

And once you find a home you want to put an offer on, pre-approval has another big perk. It not only makes your offer stronger, it shows sellers you’ve already undergone a credit and financial check. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Preapproval carries more weight because it means lenders have actually done more than a cursory review of your credit and your finances, but have instead reviewed your pay stubs, tax returns and bank statements. A preapproval means you’ve cleared the hurdles necessary to be approved for a mortgage up to a certain dollar amount.”

Translation: Pre-approval helps you make stronger, more informed decisions – and it helps you avoid missing out on a home or getting stuck on the sidelines when the right one hits the market. Because the reality is, competition might be lower these days, but desirable homes (especially the ones that are priced well) still go quickly.

3. Don’t Wait Until You’re “Ready”

Think of it this way: pre-approval doesn’t mean you’re buying a house tomorrow. It just means you’ll be ready when the time comes. And most pre-approvals are good for 60–90 days and can be refreshed easily if your plans change.

So, here’s a good place to start. Ask yourself this question: “If the perfect home came along today, would you be ready to make an offer?”

If your answer is “not quite,” then pre-approval is your next step.

Bottom Line

Pre-approval doesn’t box you in. It opens doors.

In today’s market, buyers who win aren’t the ones who wait. They’re the ones who plan. So, if you’re even thinking about buying in the next few months, get ahead of the game by connecting with your agent and a trusted lender.

They’ll help you understand what how the process works and walk you through every step along the way, so when the right home pops up, you’re ready.

More Buyers Are Planning To Move in 2026. Here’s How To Get Ready.

Momentum is quietly building in the housing market. New data from NerdWallet shows more Americans are starting to think about buying a home again. Last year, 15% of respondents said they planned to buy a home in the next 12 months. This year, that number rose to 17%.

That 2% increase might not sound like a big jump, but in a market where buyer demand has been cooling for the past few years, it’s a sign things are starting to shift. More people are feeling ready (or at least closer to ready) to take the leap and buy a home in 2026.

And if you’re in that camp and buying a home is on your goal sheet this year, this is your nudge to connect with a local agent and a trusted lender to start laying the groundwork now.

Planning To Move in Early 2026? Start with These 4 Steps

If you’re eager to get the ball rolling right away, here’s what to tackle first:

Get pre-approved. A pre-approval gives you a real understanding of your buying power and what your payment could be at today’s rates. But keep in mind, Experian says most pre-approvals are only good for 30-90 days, so this step makes the most sense as you’re ready to get serious.

Run the numbers. Look closely at all your expenses to come up with your budget. Consider what you’re spending on other bills and what your monthly mortgage payment would be once you buy. That way you go in with open eyes and you don’t stretch too far.

Define your non-negotiables. Once you know the numbers work, figure out your must-haves. This includes your desired location, commute, layout, school district, lifestyle needs, etc. Getting clear on these now makes decisions easier once you start looking at homes.

Choose your agent early. Look at reviews online and talk to multiple agents to find one you trust that you also click with. The right agent does more than show homes. They help you understand pricing, competition, timing, and strategy before you ever write an offer.

Thinking about Buying Later in the Year? This Is Still Your Window To Prepare

Even if buying feels like a late-2026 goal, this moment still matters. The buyers who feel the most confident later are usually the ones who quietly prepared earlier.

That doesn’t mean big financial commitments or major lifestyle changes. It just means setting yourself up so you’re ready when the timing is right. Here are a few low-stress ways to do that:

Work on your credit. While you don’t need to have perfect credit to buy a home, your score can have an impact on your loan terms and even your mortgage rate. So, working to bring up your score has its perks. Paying down debt now and making payments on time can help bring your score up.

Automate your savings. If you have to remember to transfer money into your homebuying savings manually, you may forget to do it. So, you may want to set up automatic transfers to drive consistency and remove the temptation to spend the money elsewhere.

Lean into your side hustles: Do you have a gig you do (or have done before) to net some extra cash? Taking on part-time work, freelance jobs, or picking up a side hustle can help give your savings a boost.

Put any unexpected cash to good use: If you get any sudden windfalls, like a tax refund, bonus, inheritance, or cash gift from family, put it toward your house fund. You’ll thank yourself later.

The common thread here? The right prep work makes a difference.

Bottom Line

If buying a home in 2026 is on your radar, let’s start the conversation today. Not to rush a decision, but to make sure you know how to get ready for your moment.

Because every move (whether it’s next year or later) is smoother when it starts with a plan. And if you need help coming up with one that works, let’s connect.

Not Sure If You’re Ready To Buy a Home? Ask Yourself These 5 Questions.

If you’re trying to decide if you’re ready to become a homeowner in the next twelve months, there’s probably a lot on your mind. You’re thinking about your finances, today’s mortgage rates, home prices, the current state of the economy, and more. And, you’re juggling how all of those things will impact the choice you’ll make. It’s a lot.

But here’s what you need to remember. While housing market conditions are definitely a factor in your decision, your own personal situation and your finances matter too. As an article from NerdWallet says:

“Housing market trends give important context. But whether this is a good time to buy a house also depends on your financial situation, life goals and readiness to become a homeowner.”

So, instead of trying to time the market, focus on what you can control. Here are a few questions that can give you clarity on whether or not you’re ready to make your move.

1. Do you have a stable job?

Buying a home is a big commitment. You’re going to take out a home loan stating you’ll pay that loan back. Knowing you have a reliable job and a steady stream of income is important and will give you peace of mind for a purchase so large.

2. Have you figured out what you can afford?

If you have a reliable paycheck coming in, the next thing to figure out is what you can afford. This depends on your budget, spending habits, debts, and more.

At this point, it helps to talk with a trusted lender. They’ll be able to tell you about the pre-approval process and what you’re qualified to borrow, current mortgage rates and your approximate monthly payment, closing costs, and other expenses you’ll want to budget for. That way, you have a good idea of what to expect.

3. Do you have an emergency fund?

As you crunch your numbers, you’ll want to make sure you have enough cash left over in case of emergency. Think about it. You don’t want to overextend on the house, and then not be able to weather a storm if one comes along. It’s not a fun topic, but it’s an important one. As CNET says:

“You’ll want to have a financial cushion that can cover several months of living expenses, including mortgage payments, in case of unforeseen circumstances, such as job loss or medical emergencies.”

4. How long do you plan to live there?

It was mentioned above, but buying a home comes with some upfront expenses. And while you’ll get that money back (and more) as you gain equity, that process takes some time. If you plan to move again soon, you may not recoup your full investment.

So, how long should you stay put in an ideal world? Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“Five years is a good, comfortable mark. If the price of your home appreciates considerably, then even three years would be fine.”

So, think about your future. If you’re going to live there for a while, it may make sense to go for it. But, if you’re looking to sell and move within a year or two because you’re planning to transfer to a new city with that promotion you’ve been working so hard for, or you anticipate you’ll need to move to take care of family, those are things to factor in.

5. Do you have a team of real estate professionals in place?

If you do, great. But if you don’t, finding a trusted local agent and a lender is a good first step. Having the right team can make figuring out everything else easier. The pros can talk you through your options and help you decide if you’re ready to make your move, or if you have a few more things to get in order first.

Bottom Line

If you want to have a conversation about the most important things you need to consider when buying a home, let’s connect.

Reasons To Be Optimistic About the 2026 Housing Market

If a move is on your radar for 2026, there’s a lot more working in your favor than there has been in a while.

After a stretch where many people felt stuck, 2026 is shaping up to be a year with more balance, more options, and more clarity for people who want to make a move. Not because the market is suddenly “easy,” but because several key conditions are shifting.

Here’s what the experts are saying you have to look forward to.

Danielle Hale, Chief Economist at Realtor.com:

“After a challenging period for buyers, sellers and renters, 2026 should offer a welcome, if modest, step toward a healthier housing market.”

“Top economists have one word to sum up the housing market for 2026: opportunity. Lower mortgage rates and a rising supply of homes are expected to open up the housing market . . . something the real estate industry and potential home buyers and sellers have been waiting for, following three years of stagnation.”

“. . . for the first time in several years, the underlying forces are finally aligned toward gradual improvement. Mortgage rates may drift down only slowly, but income growth exceeding house price appreciation will provide a boost to house-buying power — even in a higher-rate world. Affordability won’t snap back overnight, but like a ship finally catching a steady tailwind, it’s now sailing in the right direction.”

“Buyers are benefiting from more inventory and improved affordability, while sellers are seeing price stability and more consistent demand. Each group should have a bit more breathing room in 2026.”

Why Local Insight Matters More Than Ever

Just remember, while the national outlook is improving, conditions will still be different based on where you live. Some markets will move faster than others. Some will see stronger price growth. Others will remain flat. As Lisa Sturtevant, Chief Economist at Bright MLS, explains:

“Market performance will hinge on local economic conditions, making 2026 one of the most geographically divided markets we’ve seen in years.”

That’s why understanding what’s happening in your specific area is key. The national trends set the stage, but local dynamics determine how they play out for you. And that’s why you need an agent.

Bottom Line

If you want to talk through what’s expected for our local market and which trends you’ll want to take advantage of, let’s connect.

If a move is on your radar for 2026, there’s a lot more working in your favor than there has been in a while.

After a stretch where many people felt stuck, 2026 is shaping up to be a year with more balance, more options, and more clarity for people who want to make a move. Not because the market is suddenly “easy,” but because several key conditions are shifting.

Here’s what the experts are saying you have to look forward to.

Danielle Hale, Chief Economist at Realtor.com:

“After a challenging period for buyers, sellers and renters, 2026 should offer a welcome, if modest, step toward a healthier housing market.”

“Top economists have one word to sum up the housing market for 2026: opportunity. Lower mortgage rates and a rising supply of homes are expected to open up the housing market . . . something the real estate industry and potential home buyers and sellers have been waiting for, following three years of stagnation.”

“. . . for the first time in several years, the underlying forces are finally aligned toward gradual improvement. Mortgage rates may drift down only slowly, but income growth exceeding house price appreciation will provide a boost to house-buying power — even in a higher-rate world. Affordability won’t snap back overnight, but like a ship finally catching a steady tailwind, it’s now sailing in the right direction.”

“Buyers are benefiting from more inventory and improved affordability, while sellers are seeing price stability and more consistent demand. Each group should have a bit more breathing room in 2026.”

Why Local Insight Matters More Than Ever

Just remember, while the national outlook is improving, conditions will still be different based on where you live. Some markets will move faster than others. Some will see stronger price growth. Others will remain flat. As Lisa Sturtevant, Chief Economist at Bright MLS, explains:

“Market performance will hinge on local economic conditions, making 2026 one of the most geographically divided markets we’ve seen in years.”

That’s why understanding what’s happening in your specific area is key. The national trends set the stage, but local dynamics determine how they play out for you. And that’s why you need an agent.

Bottom Line

If you want to talk through what’s expected for our local market and which trends you’ll want to take advantage of, let’s connect.

Turning a House Into a Home: The Benefits You Can Actually Feel

There’s a lot of conversation about home prices, mortgage rates, and affordability right now – and those things are important. But if you’re thinking about buying a home, it’s worth remembering something the headlines rarely talk about: people don’t buy homes just for financial reasons. They buy them for their lives.

Because while homeownership can absolutely be a smart long-term financial move, it also comes with some emotional benefits spreadsheets just can’t capture. Maybe that’s why a 2025 survey from Fannie Maenotes:

“Consumers were twice as likely to mention lifestyle benefits (67%)—like security, customization, and outdoor space—than financial benefits (34%) when explaining why their homes have become more important in recent years.”

Here are a few reminders of what owning a home gives you that renting never will.

1. A Milestone You Get To Be Proud Of

Buying a home is a big deal. First home, fifth home – it doesn’t matter. It’s a moment you’ll remember. And when you finally get those keys and walk through the door, that feeling of “I did this” hits different. It’s not just a purchase. It’s an accomplishment.

2. A Place That Feels Like Your Reset Button

Life is busy. Having a place that’s truly yours where you can shut the door, take a breath, and settle into your own routine is something renters rarely talk about until they finally experience it. Home becomes the place you go to recharge, not just the place your mail is delivered.

3. Space That Fits the Way You Actually Live

Need a quiet corner for work calls? A backyard big enough for the dog that thinks it’s a person? A shorter drive to see the people who are most important to you? When you own, you get to choose a space that fits your life now and where it’s heading – and it just feels right.

4. Freedom To Make It 100% Yours

Want to paint the kitchen navy? Go for it. Thinking about a wall of floating shelves or a bold wallpaper moment? Do it. Need space for a home gym or a reading nook? Make it happen. Homeownership gives you the freedom to shape your space instead of asking for permission to change it.

Bottom Line

Buying a home isn’t only about dollars and data points – it’s about building a life you love.

So, if you’re thinking about a move in 2026, keep the emotional side in the conversation too. And when you’re ready to explore your options, let’s connect so you have a pro on your side to guide you through the process with clarity and confidence.

When your house doesn’t sell, it does more than disrupt your plans, it hits close to home. You prepared for the next chapter. You told people you were moving. You pictured where you’d go next. And then nothing happened.

It’s normal to feel frustrated, confused, or even a little embarrassed. But here’s the part you have to remember: just because your house didn’t sell the first time, doesn’t mean it won’t sell.

And here’s what most agents won’t tell you. In most cases, the difference typically comes down to the strategy behind the sale, not the house itself. And there’s real data to back that up.

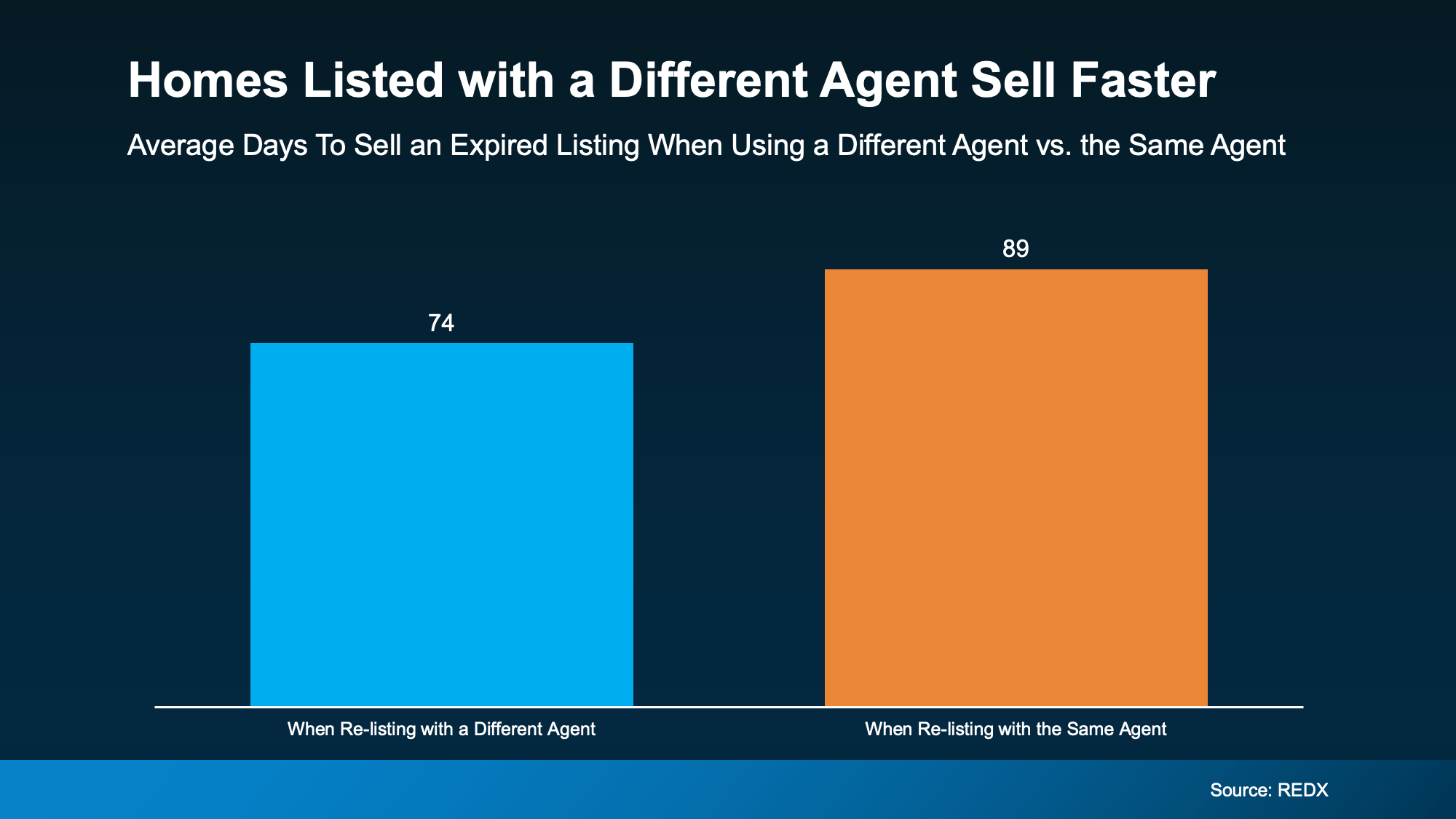

Research from REDX found over half (54%) of homeowners who re-list with a different agent end up selling their house. Re-list with the same agent? That stat drops to only 36%. You deserve better odds than that.

So, if your house didn’t sell, don’t stress. You’re not stuck. You may just need a different professional with a different approach.

Because, at the end of the day, maybe the problem wasn’t the market or your home. It was the strategy.

Let’s break down what might’ve gone wrong – and how a fresh perspective can help you have a winning plan this time.

1. The Price Was Working Against You

A lot of sellers are aiming a bit too high these days, hoping to match the price their neighbor got during the 2021 frenzy. And that’s not working anymore.

Today’s buyers are being more selective. Even a slightly overpriced home will get overlooked today. And once your listing starts to go stale, it’s hard to regain momentum. The result? A widening gap between seller and buyer expectations (see graph below). That could be what cost you your sale.

The Fix: Get a fresh pricing analysis rooted in what’s happening right now in your neighborhood – not what happened in 2021. Sometimes even a small adjustment can bring the right buyers through the door. HousingWire reports many successful sellers only had to reduce their price by about 4% to get real traction. In the grand scheme of selling a home, it’s really not that much.

2. Your House Didn’t Show Well

You only get one shot at a first impression. If the listing photos didn’t pop, the house wasn’t staged well, or it wasn’t updated, most buyers today will skip over it without ever scheduling a showing. And even if buyers did pass through, small things like scuffed walls, outdated light fixtures, or a wobbly doorknob can turn them away.

The Fix: Let’s walk through your house with fresh eyes to see if there are any areas that may have been sticking points inside and out. Sometimes simple updates (new paint, updated lighting, fresh landscaping, or better listing photos) can completely change how buyers react.

3. It Didn’t Get the Right Exposure

If your home didn’t sell, chances are it wasn’t getting the visibility it deserved. Generic flyers and a few online photos aren’t enough anymore. Today’s top agents are using highly targeted digital marketing, social media strategies, custom video content, and more to get your listing in front of the right buyers at the right time.

The Fix: We have to do more than just put your house online and hope it sells. With the right pricing, staging, and marketing, your house can still sell. It may even happen faster if you switch agents. Here’s a real-world example (see graph below):

4. You Weren’t Willing To Negotiate

In this market, flexibility matters. If you weren’t open to negotiating on repairs, closing costs, or other concessions, buyers may have walked, especially because many now expect at least some give-and-take.

The Fix: Be willing to meet buyers where they are. The goal is to get the deal done – and sometimes that means getting creative to cross the finish line. Home values have increased by 48.5% over the last five years, so you likely have enough wiggle room to offer some perks without sacrificing your bottom line.

Bottom Line

If your house didn’t sell and your listing has expired, you’re not stuck. You just need a better plan. And maybe, a better partner.

Same house. Different strategy. Completely different results.

If you’re ready to understand what held your sale back (and how to get it right this time), let’s take a fresh look together. A few strategic shifts could be all it takes to get your move back on track.

Headlines Have You Worried about Your Home’s Value? Read This.

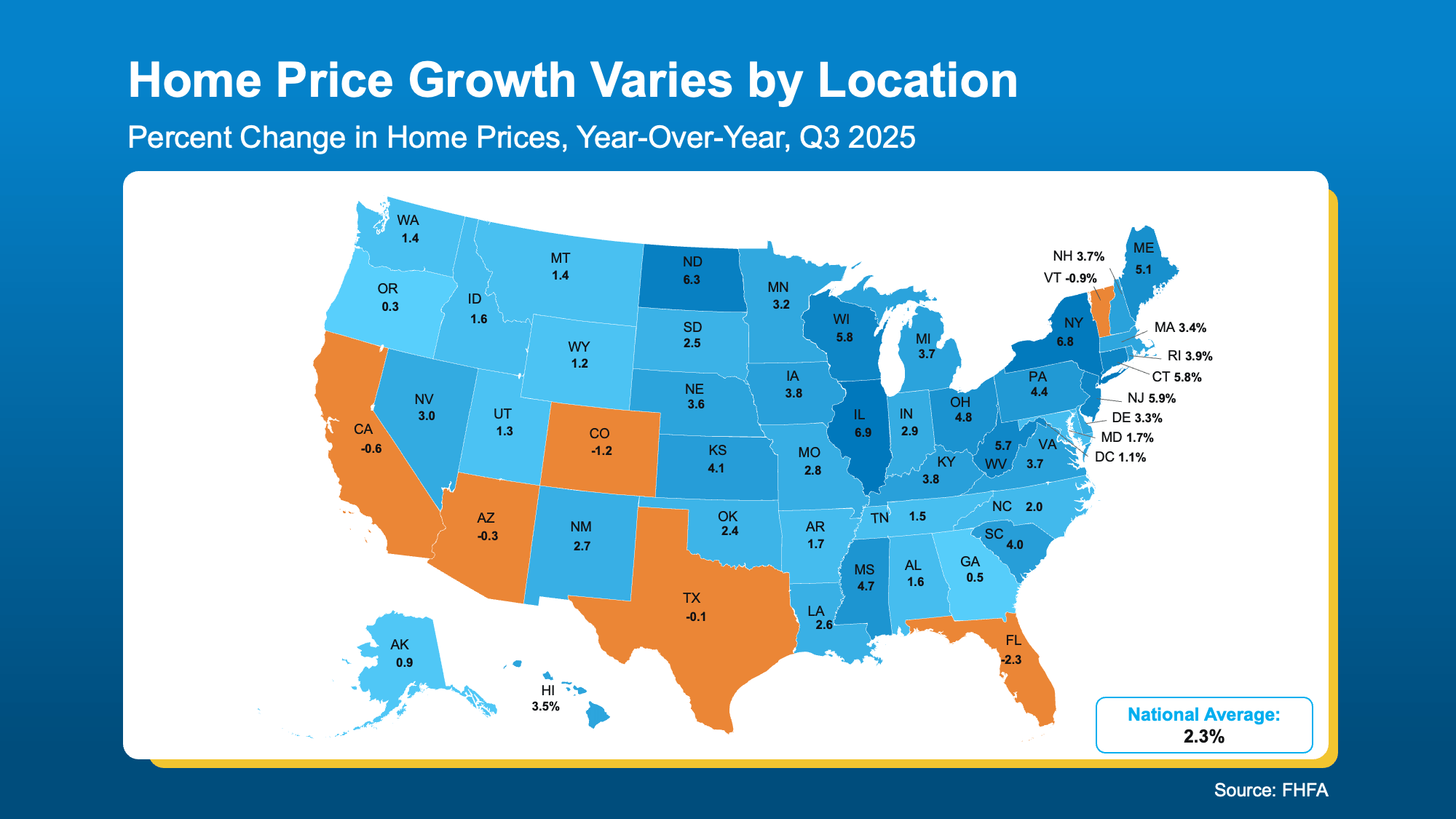

Hearing talk about home prices falling? That may leave you worried about whether your house is losing value. But here’s what you need to know. While some local markets have seen small price dips this year, home prices arenot falling nationally. So, don’t let the headlines scare you.

The vast majority of the country is actually seeing prices rise.

While that may feel surprising after the headlines you’ve seen, the map below uses year-over-year data from the Federal Housing Finance Agency (FHFA) to make that clear:

Let’s break down what this really shows.

Most states are seeing prices rise (the blue in that map). Not fall. Now, the gains aren’t as big as they’ve been in recent years, but that’s okay. The story is still, prices are growing. And that positive majority is exactly why data from the National Association of Realtors (NAR) shows, nationally, home prices are up 2.1% compared to last year.

But the headlines don’t draw attention to this. They feed on the negative. But even that isn’t as bad as it sounds.

Yes, there are some states where homes have lost value over the past 12 months (the orange in the map above). That’s what all the chatter is drawing attention too. But here’s what the data really says.

The dips aren’t happening everywhere. And in the select states where prices are inching down, it’s slight. The range here is -0.1 to roughly -2%.

And those states are the ones where prices spiked too high, too fast during the pandemic housing boom. There was always going to be a come down period after that. Now, we’re in it. In those places, prices are leveling off. And that’s a sign of normalization, not collapse.

In plain terms: Home prices aren’t crashing. And this isn’t doom and gloom or the sign of broader trouble.

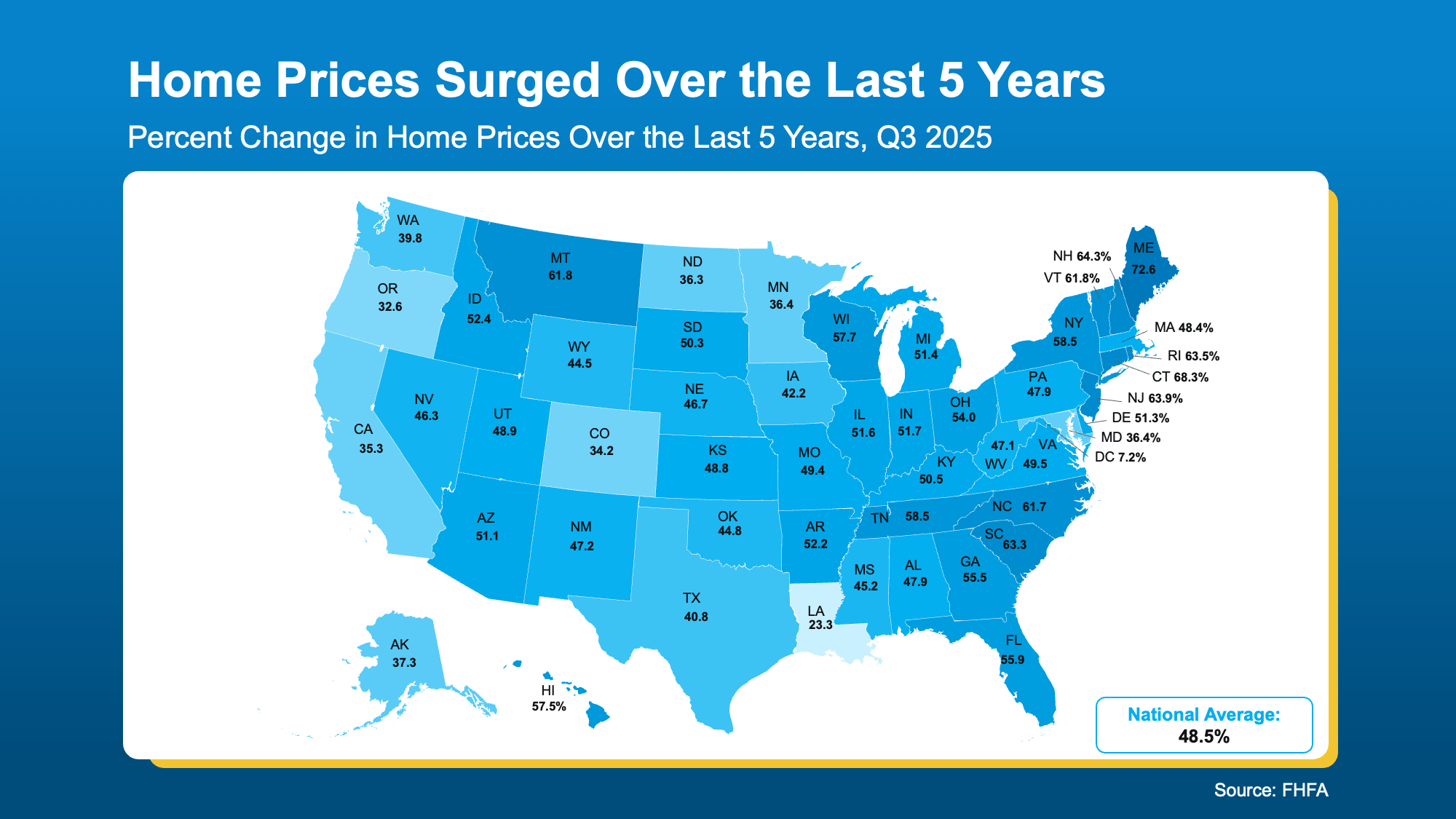

Most Homeowners Still Have Plenty of Value

Just to drive that point home, here’s one more thing to reassure you. Even in the few places where prices dipped slightly, most homeowners are still way ahead. Additional context from Zillow helps prove that point:

Only about 4% of homes are worth less than what the owner originally paid.

And 96% of homes are still worth more than their homeowners paid for them.

But don’t just take their word for it, see for yourself. When you zoom out and look at how much home prices have grown over the past five years, it’s a lot easier to understand why so many homeowners are still in such great shape.

Nationally, prices are up almost 49% in the last 5 years alone, and just about everywhere saw double-digit price growth in that time frame. That’s why there’s no orange in this map (see below):

The truth is, across the board, homeowners are still sitting on substantial gains. So, the -0.1 to -2% declines some states are seeing now? That’s easily absorbed.

So, don’t let the headlines scare you. What’s happening with home prices this year varies a lot from one area to the next. But the takeaway is clear: a small dip in some areas doesn’t mean your home’s value is collapsing.

It means select local markets are correcting – and most of the time these are the ones that saw prices rise the most during the pandemic. You’re probably still in great shape.

Bottom Line

If you’re hearing talk about price drops or crashes, a closer look at the data can help put things in perspective. That’s only happening in some markets. Most of the nation is still seeing prices rise.

And for the vast majority of homeowners, the long-term gains far outweigh any recent softening.

If you want help understanding what’s happening in our local market, let’s connect.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

So, even if your score isn’t as high as you want, that doesn’t automatically close the door. FICO explains there is no universal credit score you absolutely have to have when buying a home:

So, even if your score isn’t as high as you want, that doesn’t automatically close the door. FICO explains there is no universal credit score you absolutely have to have when buying a home:

How an Agent Can Help

How an Agent Can Help

The Fix: Get a fresh pricing analysis rooted in what’s happening right now in your neighborhood – not what happened in 2021. Sometimes even a small adjustment can bring the right buyers through the door. HousingWire reports many successful sellers only had to reduce their price by about 4% to get real traction. In the grand scheme of selling a home, it’s really not that much.

The Fix: Get a fresh pricing analysis rooted in what’s happening right now in your neighborhood – not what happened in 2021. Sometimes even a small adjustment can bring the right buyers through the door. HousingWire reports many successful sellers only had to reduce their price by about 4% to get real traction. In the grand scheme of selling a home, it’s really not that much. 4. You Weren’t Willing To Negotiate

4. You Weren’t Willing To Negotiate