Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

You may be telling yourself you’re going to wait to move – maybe you’re hoping mortgage rates will come down, prices will fall, or the market will feel a little easier.

And honestly? A lot of people feel that way right now. But here’s what some are starting to realize.

Waiting doesn’t usually fix the thing that made you want to move in the first place.

Your family still desperately needs more room. Your empty nest still feels too…empty.

Your parents or grandparents still need you to live closer.

You just got married… or divorced.

Your vision of retirement has you living somewhere else.

Eventually, life can reach a point where waiting feels harder than moving.

That’s why some people are still deciding to buy right now, even in today’s market. Not because conditions are perfect. But because the life changes behind their move never really went away.

And maybe that’s exactly where you are too. If so, you’re certainly not alone.

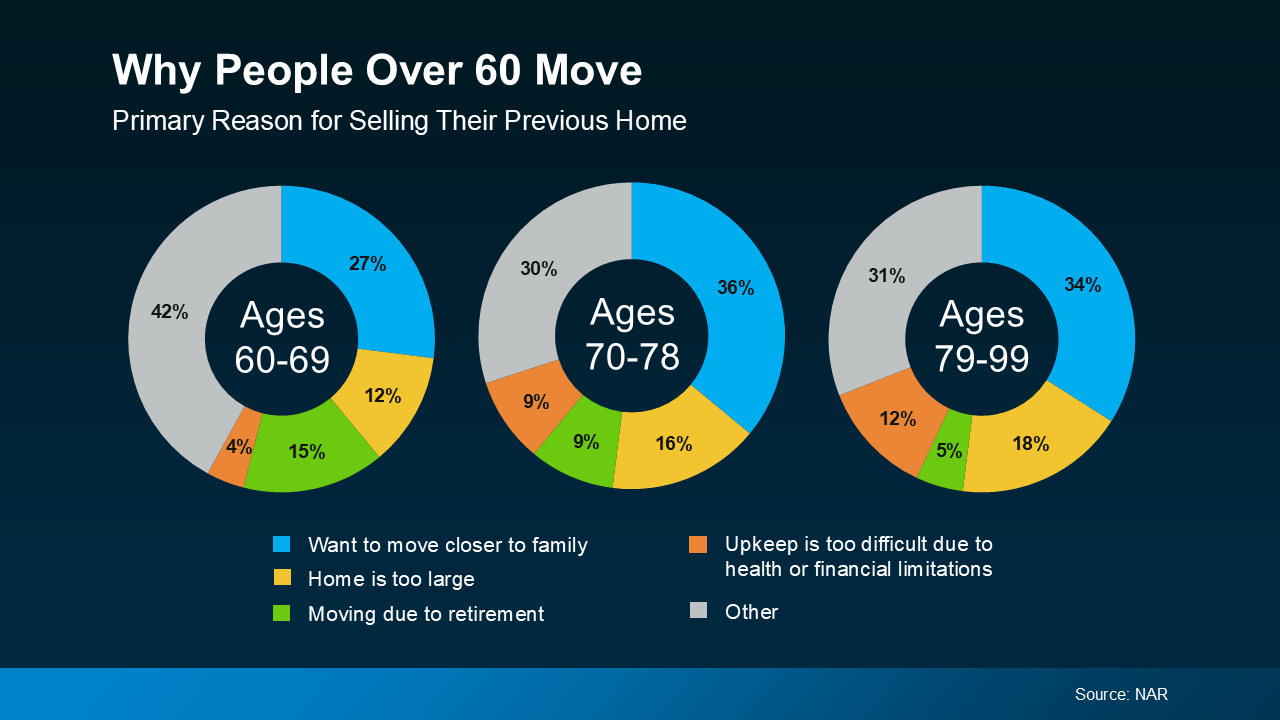

The Real Reasons People Move

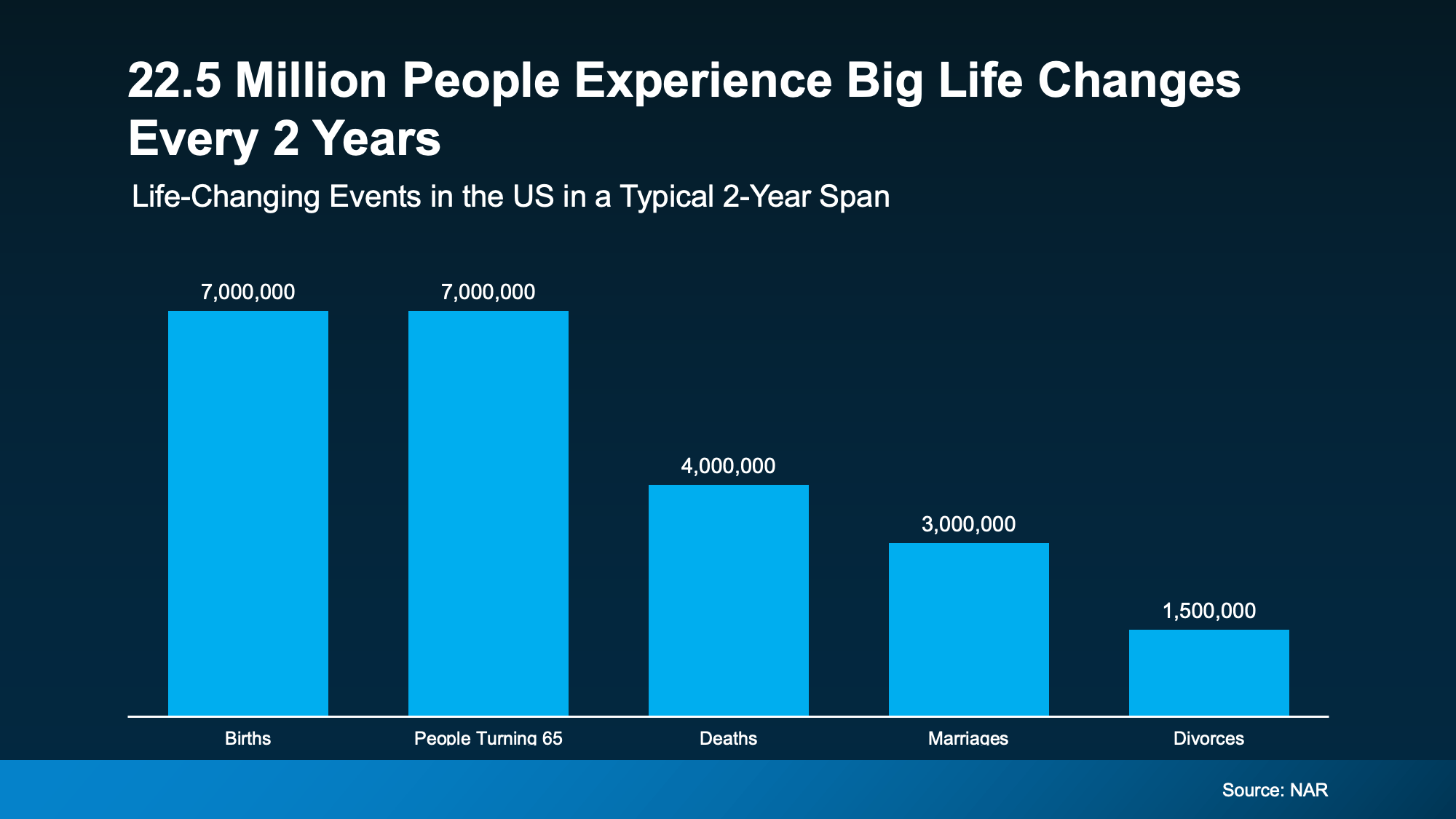

Data from the National Association of Realtors (NAR) shows 1 in 5 buyers last year said they felt like they had to purchase a home at that time, no matter the market.

That’s an important reminder right now. Sure, the dollars and cents of your move have to make sense for you. But big life changes happen whether mortgage rates and home prices are high, low, or somewhere in between.

And those big life events happen more than you may think. NAR says roughly 22.5 million people experience major life changes in a typical two-year span (see graph below):

These are exactly the kinds of things that can change how much space you need, where you want to live, or what kind of lifestyle makes sense now. Chen Zhao, Head of Economics Research at Redfin, explains:

“Life doesn’t stand still—people get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood.”

And that’s what makes waiting so hard. Every month you spend hoping the market changes is another month living in a house that no longer works for your life. It’s stressful to feel stuck. And that feeling usually doesn’t disappear.

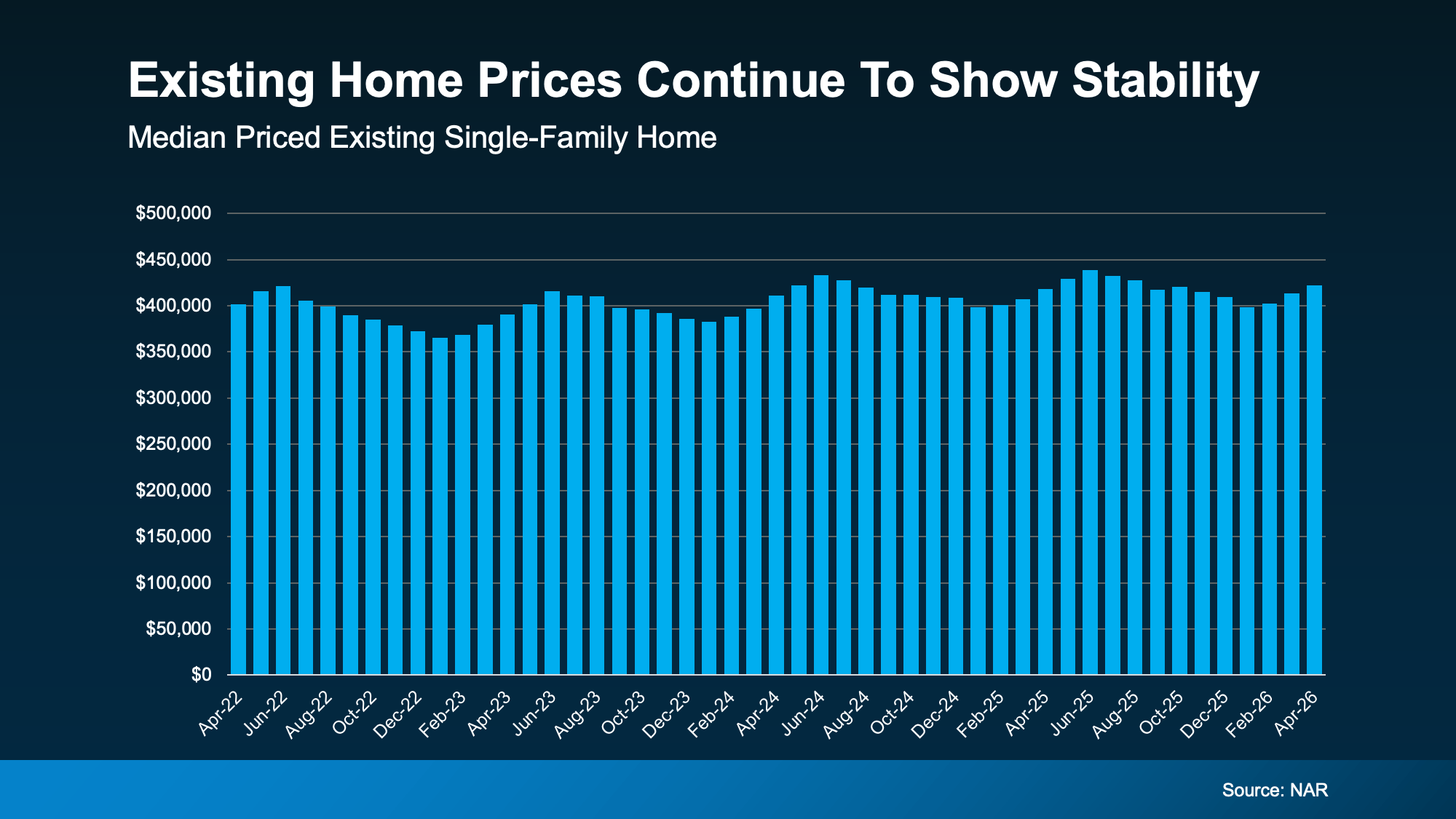

There May Be More Opportunity Than You Think

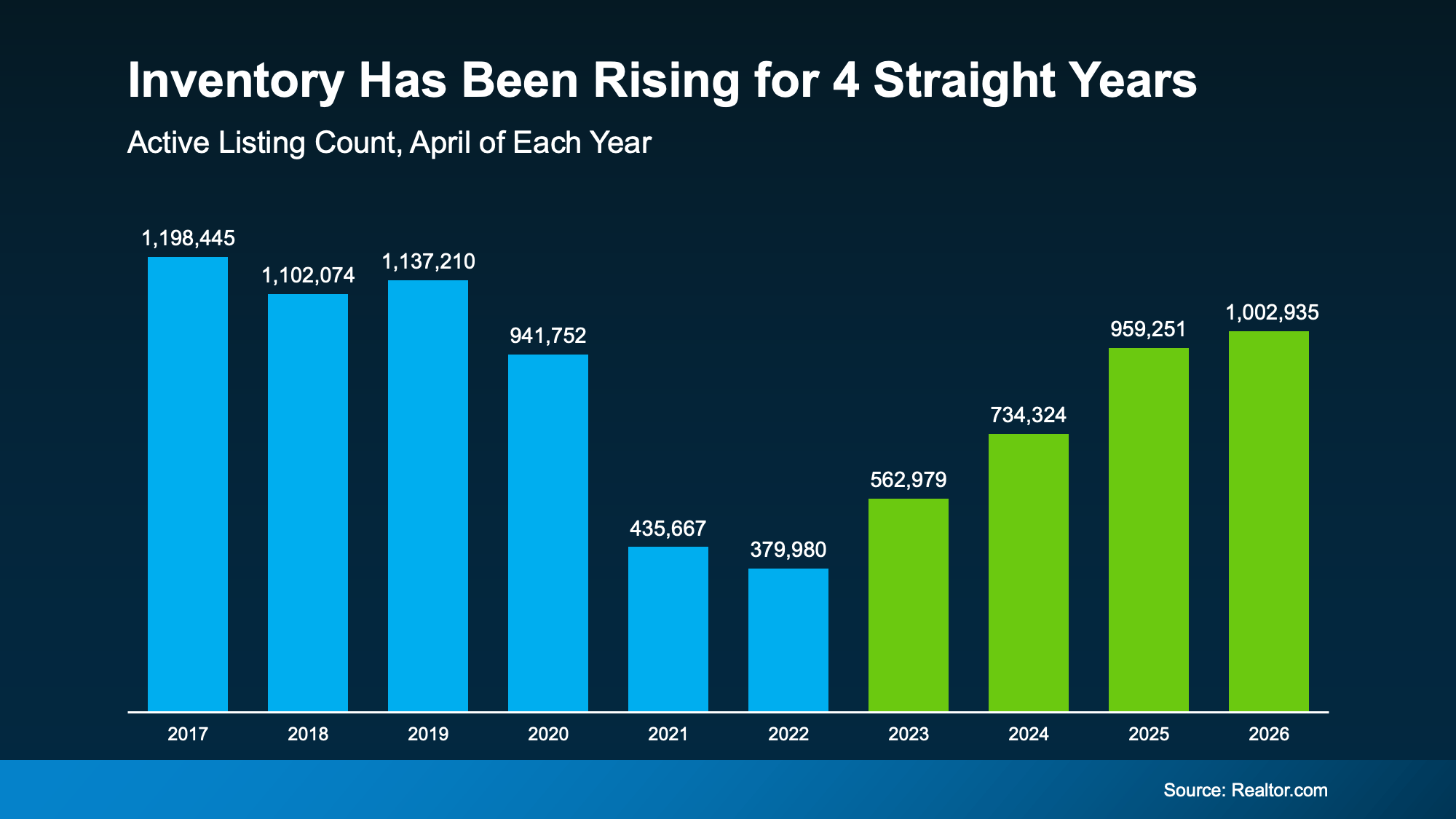

But while affordability is still a challenge, there may still be a way for you to make your move.

The number of homes for sale has been growing for 4 straight years (see graph below). That means more homes to choose from and, in some markets, more room to negotiate than buyers had just a few years ago.

That doesn’t mean moving is suddenly easy. But it does mean some buyers are finding ways to make a move work. So, if you’ve been putting your plans on hold, maybe the question isn’t just:

“What’s the market doing?” or “When will it get better?”

Maybe ask yourself this, too: “Can I still live where I’m at right now and make it work?”

If the answer to that second question is “no,” it may be worth having a conversation about what your options look like today – despite where rates or prices are. You could find your move is still possible after all. With more homes for sale, there’s a better chance to find one that fits your life (and your budget) right now.

Bottom Line

Life changes. Priorities shift. Families grow. Kids move out. Careers evolve. And eventually, the house you’re in may stop fitting the life you’re living.

If that’s been weighing on you lately, let’s talk through what your options could realistically look like today, no matter where rates or prices are.

Life can’t always wait for perfect market conditions. Maybe you don’t have to either.

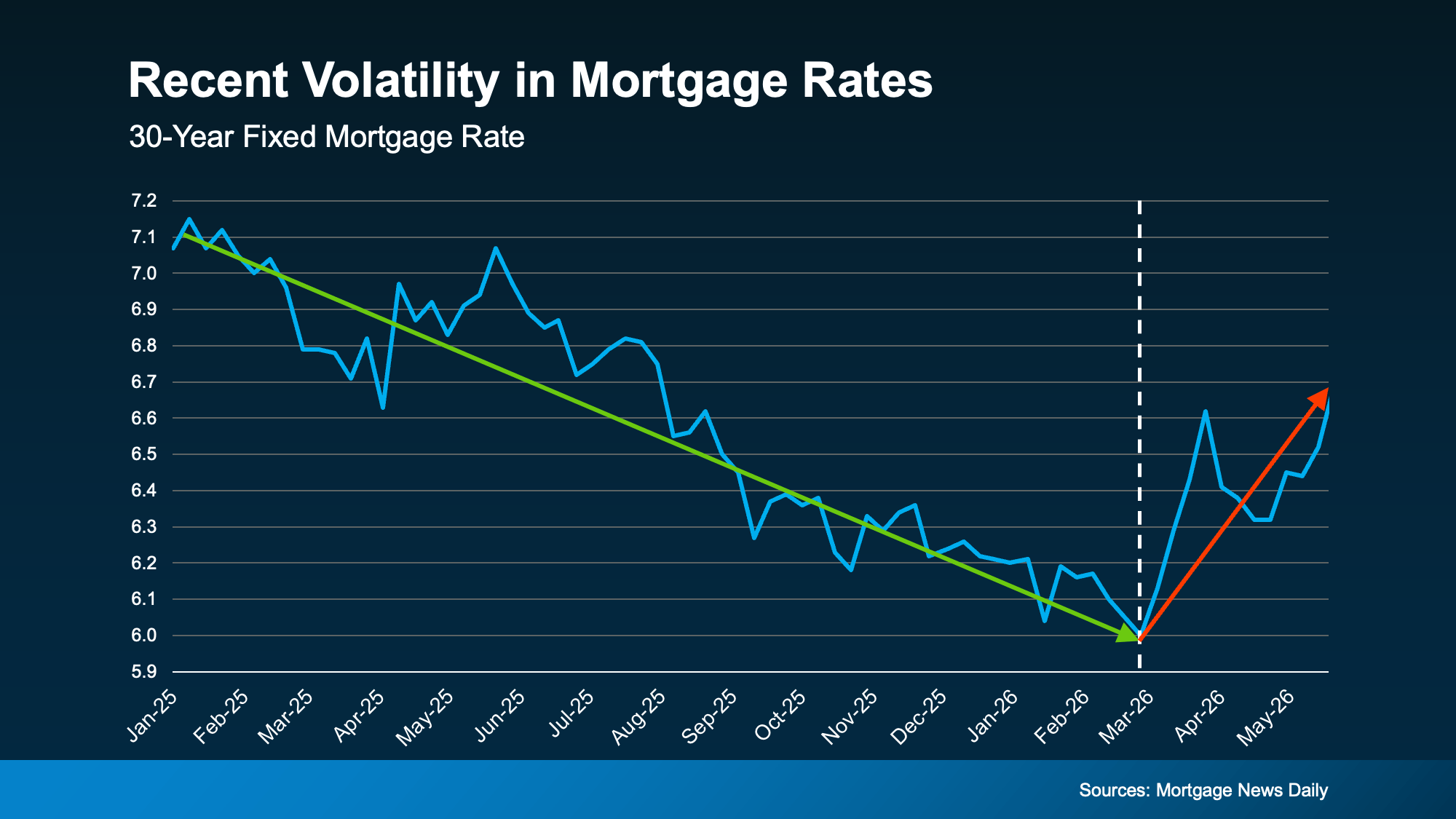

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it’s probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it’s probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

The Part Sellers Don’t See Coming

The Part Sellers Don’t See Coming